There is a striking paradox in advertising today. Ask almost any CMO, brand director, media lead, or agency executive, and they will tell you that trust has become a strategic priority. Consumers read reviews, look for proof, compare, and validate before they buy. They put more weight on other consumers’ experiences than on advertising claims alone. This is now widely accepted as fact.

Yet open any marketing budget and a different reality appears. Trust is almost never on it.

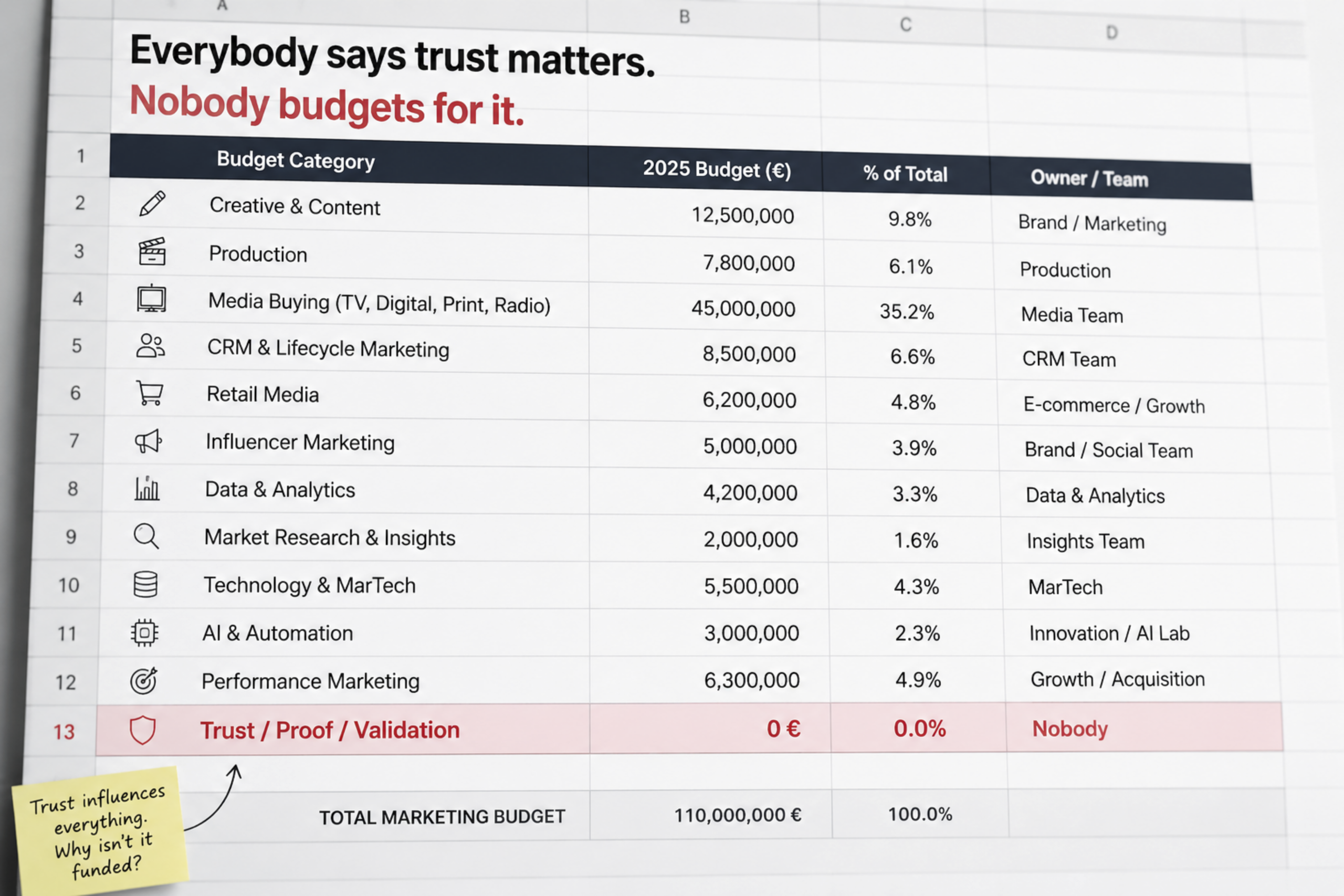

1. Everyone believes in trust. Almost no one funds it.

The budget lines are well known.

- Creative

- Production

- Media buying

- CRM

- Retail media

- Influence

- Data

- Research

- AI

- Performance

But where is the line called Trust, Proof, or Validation? Almost nowhere. Trust is assumed to improve every other line. But it almost never exists as an identified investment in its own right.

This may come down to how the market still perceives it. For many professionals, trust isn’t an activatable lever. It’s treated as the byproduct of a broader posture: product quality, brand consistency, accumulated reputation, advertising territory, customer experience, and message coherence over time.

In other words, trust is seen as something built indirectly, almost organically — rarely something that can be isolated, activated, measured, or reinforced through a specific media mechanism.

This is where the contrast with attention becomes interesting. Attention, by comparison, has been progressively broken down, modeled, quantified, sold, and optimized. The industry talks in seconds of attention, completion rates, viewability, recall, exposure time. It has learned to treat a few moments of mental availability as a full economic resource — turning those few seconds into a central battleground, in an era that media theorist Bruno Patino has described as the age of the goldfish, where attention spans keep shrinking.

Trust, on the other hand, remains far less instrumented. Everyone knows it matters, that it shapes decisions, that it conditions how messages land. But it is rarely treated as an activatable layer of media performance.

This is probably one of the industry’s most interesting paradoxes: everyone agrees trust is strategic, but very few organizations know where to place it in a budget, a media plan, or a measurement model.

2. Trust belongs to no one.

Why does trust remain so hard to turn into an actual investment? Perhaps because, in practice, it belongs to no single team.

Inside the advertiser’s organization, trust is everywhere… but rarely anyone’s direct responsibility.

- Product teams work on quality.

- CRM manages the customer relationship.

- Consumer Experience teams improve the journey.

- Communications builds reputation.

- Marketing develops brand territory.

- Agencies imagine campaigns.

- Sales houses commercialize media.

- Research institutes sometimes measure it.

- Platforms exploit it in their algorithms.

Everyone contributes to building trust. But no one truly owns it. There is generally no head of trust, no dedicated budget, no shared metric capable of managing trust as an economic asset in its own right.

This fragmentation may explain why trust so often ends up as a consequence rather than an operational objective.

This situation is all the more paradoxical given that the industry is constantly searching for new sources of credibility. Influencers are a good example. For several years, they answered the growing distrust of traditional advertising through a relationship with their communities perceived as more personal and authentic.

But as commercial partnerships multiply, their role is shifting too. They are becoming progressively integrated into the advertising economy itself. In other words, they are no longer just content creators — they are also becoming ad formats.

This evolution isn’t abnormal. It’s even logical. But it points to a deeper truth: no channel, no spokesperson, and no format enjoys a permanently inexhaustible reserve of trust. Trust cannot be declared. It is built, verified… and renewed.

This may be the real challenge of the coming years. If trust belongs neither to brands, nor to agencies, nor to media, nor even to content creators, then it becomes a collective asset that the industry has to learn to organize.

And it is precisely because it belongs to no one today that trust still struggles to earn its own budget line. When an asset has no clearly identified owner, it rarely becomes a priority investment.

3. Premium and participation are not incompatible.

This may be where one of the industry’s last great misconceptions still lives.

Over the past fifteen years, consumer reviews have become embedded across many sectors. They are now nearly unavoidable in travel, hospitality, restaurants, electronics, retail, automotive, financial services, and even healthcare, where they directly influence purchase decisions.

Yet in the most premium categories, the picture looks very different. Luxury houses, fine watchmaking, jewelry, high-end automotive brands, and many heritage brands rarely put customer reviews at the center of their brand experience or communications.

As if premium and participation belonged to two incompatible worlds. This perception is understandable. For a long time, reviews were associated with marketplaces, price comparison sites, e-commerce product pages, and transactional platforms. In that world, the logic is primarily functional: compare, reassure, decide.

The premium territory follows a different logic. It seeks to build desirability, rarity, emotion, brand culture, and imagination. The fear is natural: would bringing consumer reviews into that world dilute it?

The question is worth asking. But it may rest on a misunderstanding. A review does not, on its own, determine whether a piece of communication is premium or not. It is the creative execution, the media context, and the editorial craft that give it meaning and value.

A handful of authentic experiences, curated by a brand and its agency and woven into a demanding creative or editorial environment, have nothing in common with a wall of comments on a product page. The media, the creative, and the art direction fundamentally change the nature of that proof.

In other words, premium is not the opposite of reviews. It may in fact be exactly what gives them their strongest value. Premium media have always known how to select, editorialize, and contextualize content. Why couldn’t the same logic apply tomorrow to certain forms of consumer proof?

What if the real question were no longer: “Can premium brands display reviews?” But rather: “How can premium brands turn a handful of authentic proof points into a new communications asset, without giving up their brand territory?”

Conclusion

For years, the industry has built increasingly sophisticated infrastructures for distribution, targeting, measurement, and optimization. Trust, meanwhile, is still largely treated as a byproduct.

What if the real challenge of the coming years were to give it its own economic status? Not as a vague promise or a secondary KPI, but as an identifiable layer of value creation.

AdTrust’s first cycle explored one idea: trust could become infrastructure. The second begins with another question: why doesn’t a resource everyone considers essential have its own budget line yet?

Everything that creates durable value eventually earns its own line in the budget. The real question may no longer be whether trust deserves a budget… but when.

This question deserves a wider debate across the industry. AdTrust will keep exploring this territory in the editorial cycles ahead.